1. Executive Summary

In 2026, three structural shifts are reshaping demand for metal shredder wear parts simultaneously: scrap volumes are rising, ELV regulations are tightening across Europe and Asia, and circular economy compliance has moved from voluntary to mandatory in major markets.

Wear parts — hammers, liners, grates, anvils, pin protectors, and pusher bars — are the consumable backbone of every automobile shredder. They wear down predictably, they must be replaced on schedule, and deferring replacement stops operations. This non-discretionary replacement cycle, combined with the rising throughput volumes described in this report, defines the market’s growth trajectory.

Key findings at a glance:

| Indicator | Value | Source |

| Global metal shredder market size (2026) | ~USD 1.4 billion | Business Research Insights ¹ / Grand View Research ¹ᵃ |

| Projected size (2030–2035) | USD 1.95–2.3 billion | Business Research Insights ¹ / Grand View Research ¹ᵃ |

| Global scrap metal recycling market (2026) | USD 458.70 billion (commodity value) | Precedence Research ² |

| Global vehicle recycling market CAGR (2026–2035) | 12.8% | Market.us ³ |

| Vehicles recycled globally per year | ~27 million | OICA / Market.us ³ |

| Asia Pacific market share (scrap metal recycling) | ~48% | Precedence Research ² |

Wear Parts Sub-Market Note: No major research firm publishes the metal shredder wear parts segment as a standalone category. Based on the industry benchmark that wear parts represent 15–25% of total shredder lifecycle costs, the addressable wear parts market is estimated at approximately USD 425–710 million in 2026. This is a derived figure with no independent verification — see Section 2.1 for full methodology.

2. Market Size & Growth Forecast

2.1 Industrial Shredder Equipment Market

The global metal shredder equipment market is valued at approximately USD 1.4 billion in 2026, based on estimates from Business Research Insights (USD 1.418B) and Grand View Research (USD 1.408B for 2024, projected forward) ¹ ¹ᵃ. The market is forecast to reach approximately USD 1.95–2.3 billion by 2030–2035 at a CAGR in the 5–6% range ¹ ¹ᵃ.

A note on market sizing discrepancies: Some industry sources cite a significantly larger figure of ~USD 2.85B for the industrial shredder market. This discrepancy likely reflects broader scope definitions that include adjacent equipment categories (e.g., industrial granulators, shredder-baler systems, or the full shredding line rather than the primary shredder unit alone). The USD 1.4B figure from Business Research Insights and Grand View Research is used here as it is traceable to verifiable commercial research reports.

Within the primary shredder segment — large-scale hammermill machines used for automobile and scrap metal processing — global sales reached approximately 3,300 units in 2025 at an average price of USD 122,000 per unit. QYResearch projects this primary shredder segment will reach USD 622 million by 2032 (CAGR: 6.8%) ⁵. In the United States specifically, the crusher and shredder machine market is growing at 5.5% annually through 2033 ⁴.

Wear Parts Sub-Market Sizing Note: Dedicated market data for the metal shredder wear parts sub-segment does not exist as a standalone published category. The widely cited industry benchmark — that wear parts account for 15–25% of total shredder lifecycle costs — yields a directional estimate of USD 425–710 million for the addressable wear parts market in 2026. This figure is derived from the industrial shredder market size above and has not been independently verified by any third-party research firm as of April 2026. It should be treated as an order-of-magnitude reference only.

2.2 Upstream Scrap Metal Recycling Market

Shredder wear parts consumption is, at its core, a function of tonnage throughput. The upstream scrap metal recycling market sets the structural ceiling for wear parts demand.

A note on data scope variance: Market sizing figures for scrap metal recycling vary significantly across research providers because they measure fundamentally different things. Precedence Research’s USD 458.70B figure represents the total commodity value of scrap metal traded and processed globally. Coherent Market Insights’ USD 67.40B figure represents industry revenue from recycling operations — equipment sales, processing fees, and labor — which is a narrower scope. For wear parts market sizing purposes, neither figure is directly applicable; throughput tonnage is the more relevant metric, which we address in Section 8.

| Metric | Value | Source |

| Global scrap metal recycling market (2026) — commodity value | USD 458.70 billion | Precedence Research ² |

| Projected market size (2035) | USD 722.65 billion (CAGR: 5.18%) | Precedence Research ² |

| Global scrap metal recycling — operations revenue (2026) | USD 67.40 billion | Coherent Market Insights ⁶ |

| Projected operations revenue (2033) | USD 100.70 billion (CAGR: 5.9%) | Coherent Market Insights ⁶ |

| US Scrap Metal Recycling industry size (2026) | USD 40.0 billion | IBISWorld ⁷ |

2.3 Vehicle Recycling Market

Market.us values the global vehicle recycling market at USD 97.5 billion in 2025, projecting growth to USD 325.2 billion by 2035 at a CAGR of 12.8% ³. A separate estimate from LinkedIn Industry Insights puts the ELV recycling segment at USD 11.22 billion in 2025 with a CAGR of 11.33% through 2033 ⁸, likely reflecting processing-only revenue.

The 12.8% vehicle recycling CAGR is the single most important macro signal for wear parts demand planning. It suggests significant throughput growth through 2035 — though it bears noting that dollar-value CAGR incorporates price effects alongside volume growth; actual shredder throughput in tonnage terms will grow at a more moderate rate.

3. Key Market Drivers

3.1 End-of-Life Vehicle Volumes Are Structurally Rising

Approximately 27 million vehicles are recycled globally each year (OICA) ³. That number is not a plateau — it is a floor. The vehicle fleet cohorts from the high-production years of the 2000s and 2010s are now entering end-of-life windows, and annual ELV volumes are accelerating as a result.

The mechanics for wear parts are direct. Each vehicle processed imposes predictable mechanical stress on hammers, liners, and grates. A typical automobile shredder processing 200–400 tons per hour requires hammer replacement every 500–2,000 operating hours, depending on alloy grade and feedstock hardness. More ELV throughput means more replacement cycles — there is no operational workaround.

3.2 EAF Steelmaking Is Expanding Scrap Demand

The steel industry’s decarbonization trajectory structurally favors electric arc furnace (EAF) production, which uses scrap metal as its primary feedstock. As EAF capacity expands — driven by net-zero commitments across Europe, North America, and increasingly Asia — demand for processed scrap increases with it.

Ferrous metals currently represent approximately 75% of the scrap metal recycling market by value ². The automotive segment is growing at the fastest end-use CAGR of 4.7% through 2035 ². Every ton of automotive-grade scrap that an EAF mill consumes was processed through a hammermill — and every processing hour consumes wear parts.

3.3 Regulatory Mandates Are Accelerating Shredding Capacity Investment

Regulation is compressing the timeline for ELV processing infrastructure investment across multiple major markets:

- EU ELV Regulation (ST-6759-2026):The European Council’s updated ELV framework establishes mandatory obligations for ELV collection, treatment, and material recovery ⁹, superseding Directive 2000/53/EC. EU vehicles must achieve 85% reuse and 95% recyclability targets ¹⁰.

- EU Circular Economy Action Plan:Targets 65% municipal waste recycling, directly driving investment in shredding infrastructure ⁵.

- India ELV Policy (2026):NITI Aayog’s report introduces composite incentive packages — scrap value payments, automaker discounts, and waived registration fees ¹¹ — expected to dramatically expand formal scrapping capacity in South Asia’s largest automotive market.

- Carbon Neutrality Commitments:Industry commentary citing the Global Recycling Association’s 2024 report indicates that global demand for scrap metal shredding equipment is growing at approximately 12% annually, driven specifically by carbon neutrality targets ¹².

3.4 Non-Ferrous Recovery Is Creating New Demand Vectors

The non-ferrous metal recycling market is valued at approximately USD 124.8 billion in 2026 ¹³.

Data scope note: Some sources cite figures near USD 249B for non-ferrous metal recycling. This higher figure typically includes primary (virgin) non-ferrous metal production and trading alongside recycled metal flows, significantly broadening the scope. The USD 124.8B figure reflects recycling operations revenue only and is used here for consistency with other recycling market metrics in this report. Aluminum scrap recycling alone is projected to reach USD 48.6 billion by 2030 at a CAGR of 9.8% ¹⁴. The EV transition is accelerating this trend: ORNL projects up to 350,000 tons of EV-sourced aluminum body sheet scrap in North America entering recycling streams by the early 2030s ¹⁵. Processing aluminum-intensive EV bodies creates different technical demands for shredder wear parts — distinct impact profiles and abrasion characteristics compared to traditional steel-heavy vehicles.

4. Regional Market Analysis

4.1 Asia Pacific — Volume Leader

Asia Pacific holds approximately 48% of the global scrap metal recycling market ² and 49.2% of the global vehicle recycling market, generating USD 47.9 billion in 2025 ³. Growth in the region is driven primarily by China’s expanding EAF steelmaking capacity and scrap processing infrastructure. India’s new ELV incentive framework ¹¹ is formalizing a previously fragmented scrapping sector — representing new capacity investment that will translate directly into wear parts demand. Japan and South Korea maintain mature automotive recycling ecosystems with high per-vehicle recovery rates. On the supply side, the growing Chinese domestic wear parts manufacturing base — concentrated in Shandong province and the Shanghai region — positions Asia Pacific producers to serve both regional and global aftermarket demand at competitive cost structures.

4.2 North America — Fastest Growing

North America is projected to grow at the fastest CAGR in scrap metal recycling between 2026 and 2035 ². The US scrap metal recycling industry alone is valued at USD 40.0 billion in 2026 (IBISWorld) ⁷, with the crusher and shredder machine market growing at 5.5% annually through 2033 ⁴. The region’s large installed base of Newell, Hammermill, and Metso-type shredders — operated by large EAF steelmakers including Nucor, Steel Dynamics, and Commercial Metals Company — generates consistent, high-volume OEM and aftermarket wear parts demand. EPA compliance requirements and growing state-level circular economy regulations are adding incremental pressure to upgrade processing equipment and throughput efficiency.

4.3 Europe — Regulatory-Driven Investment Cycle

Europe’s industrial shredder market is projected to grow at 6.8% CAGR ¹⁷ — above the global average — driven by the EU’s updated ELV Regulation and Circular Economy Action Plan. The EU’s incoming recycled-content quotas for metals, plastics, and battery materials are compelling recyclers across Germany, France, Spain, and the Netherlands to invest in higher-capacity shredding operations ¹⁸. ERTRAC’s 2026 deep-dive on ELV recycling in the EU confirms that existing legal targets are being superseded by more ambitious recovery mandates ¹⁹ — a regulatory escalation that directly increases throughput requirements and, therefore, wear parts consumption per year.

5. Competitive Landscape

5.1 Two-Tier Market Structure

The metal shredder wear parts market operates on a clearly defined two-tier structure.

Tier 1 — OEM & Premium Suppliers (brand-specific fitment, engineered alloys, premium pricing):

- Metso— Global leader in crushing and shredding equipment; supplies OEM wear parts with proprietary alloy compositions developed over decades of field testing.

- K2 Castings— Specialized American supplier of shredder hammers and wear parts for automobile shredder applications.

- AMSCO Wear Parts— Major US-based manufacturer of shredder wear parts and castings; one of the oldest names in the sector.

- Wendt Corporation— Provides integrated shredder systems alongside associated wear parts programs.

Tier 2 — Aftermarket & Third-Party Manufacturers (broad brand compatibility, cost-competitive):

- HuaSheng Casting— Full-range custom-designed castings compatible with all major automobile and scrap metal shredder brands; proprietary alloy and manganese compositions; supplies leading global shredder manufacturers directly ²⁰

- Mayang Casting— Manganese steel shredder hammers for metal recycling applications ²¹

- Wujing Casting— 35+ years in manufacturing; produces Mn13–Mn22 manganese steel and high-chrome iron (Cr20+) wear parts ²³

- Sunwill Foundry— International aftermarket supplier specializing in alloy castings ²⁴

- Dingsheng Casting— Metal recycling-focused wear parts supplier ²⁵

- Qiming Casting— Alloy steel wear-resistant parts for metallurgical and recycling machinery

Major Wear Parts Buyers (large-volume operators): Sims Metal Management, Nucor Corporation, Commercial Metals Company, Schnitzer Steel Industries, Steel Dynamics, European Metal Recycling Ltd., SA Recycling ⁶

5.2 Competitive Dynamics

The cost gap is real. Qualified Chinese Tier 2 manufacturers offer OEM-compatible specifications at 30–50% below OEM pricing, with documented fitment for Newell, Metso, Hammermill, and other major shredder platforms. As recycling operators face margin pressure from scrap price volatility, qualified aftermarket sourcing is increasingly a strategic procurement decision rather than a compromise.

Proprietary alloy development is the primary differentiator. Suppliers investing in DHT alloy compositions, Mn13CrMo grades, and ceramic-insert casting technologies command pricing that bridges the OEM/aftermarket gap. Operators running high-throughput operations measure cost per ton processed, not cost per part — an extra 500 operating hours per hammer set eliminates one full change-out cycle, saving labor, crane time, and lost production.

Quality certification is becoming a buyer requirement. A well-documented dynamic in the Chinese wear parts manufacturing sector is race-to-the-bottom price competition, where aggressive cost pressure leads some producers to substitute lower-grade raw materials and reduce quality control rigor. Industry observers have termed this the “involution trap” ²⁶. The result is that premium global buyers are actively shifting toward suppliers with traceable material sourcing, documented alloy verification, and third-party certification — creating a quality bifurcation within the Tier 2 segment itself.

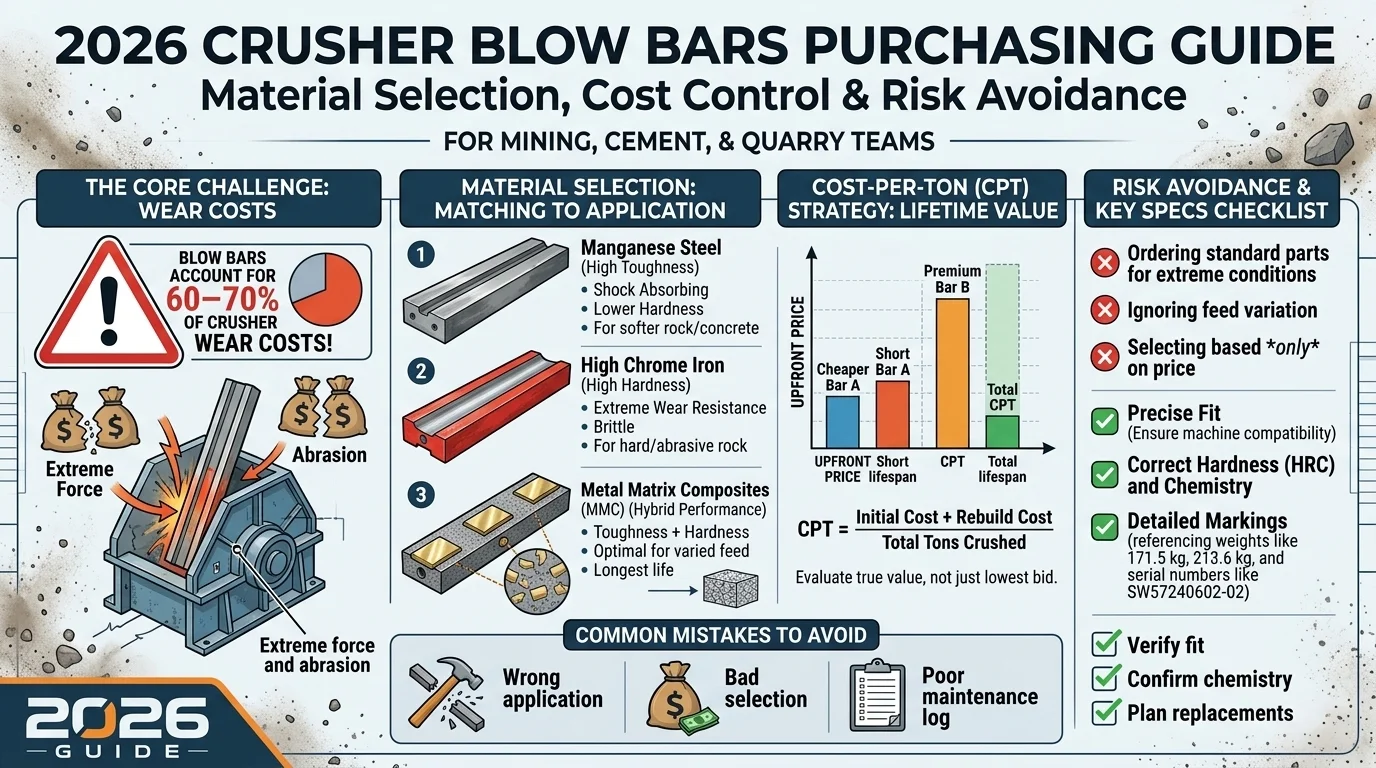

6. Product Type Analysis

6.1 Wear Parts by Component

Every automobile shredder contains multiple wear part categories, each with distinct wear mechanisms, replacement intervals, and material requirements.

| Component | Function | Primary Materials | Est. Replacement Interval |

| Hammers | Primary impact element; direct contact with scrap | Mn13, Mn13CrMo, DHT Alloy, 42CrMo | 500–2,000 hrs |

| Shell Liners | Protect shredder housing from secondary wear | High Mn Steel, High Chrome Iron | est. 2,000–5,000 hrs |

| Discharge Grates | Control output particle size; continuous abrasion | Mn13, Mn13CrMo | est. 1,000–3,000 hrs |

| Anvils / Breaker Bars | Secondary impact surface; absorbs hammer energy | High Mn Steel, Alloy Steel | est. 2,000–4,000 hrs |

| Pin Protectors / Caps | Protect hammer pin assemblies | Mn13, Mn13CrMo | 500–2,000 hrs |

| Pusher Bars | Feed material into the shredding chamber | Alloy Steel | est. 4,000–8,000 hrs |

| Cutter Bars | Assist in secondary size reduction | High Chrome Iron | est. 2,000–4,000 hrs |

Hammer replacement interval sourced from industry operational data ²⁰. Intervals for other components are indicative estimates based on operator-reported data; actual intervals vary by feedstock composition, shredder model, and operating intensity.

Hammers dominate replacement spend. As the primary impact element in every shredding cycle, hammers sustain the highest wear rates and require the most frequent replacement — making them the largest single line item in wear parts procurement budgets ²⁰.

6.2 Industry-Standard Alloy Specifications

The following material grades are the established industry standards for automobile shredder castings ²⁰:

| Grade | C% | Mn% | Cr% | Mo% | Ni% | Primary Applications |

| Mn13 | 1.03–1.17 | 12.5–14.0 | — | — | — | Hammers, Anvils, Grates, Pin Protectors |

| Mn13CrMo | 1.1–1.22 | 12.5–14.0 | 0.48–0.70 | 0.43–0.57 | — | Hammers, Anvils, Grates, Pin Protectors |

| 42CrMo | 0.38–0.45 | 0.50–0.80 | 0.90–1.20 | 0.15–0.25 | — | Hammers, Caps |

| DHT Alloy | 0.49–0.50 | 0.6–0.8 | 0.9–1.2 | 0.55–0.65 | 1.15–1.25 | Hammers only (premium grade) |

7. Material Technology Trends

The materials science of shredder wear parts has advanced substantially over the past two decades. Each generation of material development targets the same outcome: more tons processed per part replaced.

7.1 High Manganese Steel (Hadfield Steel) — The Established Baseline

High manganese steel containing 13–14% Mn — commercially known as Hadfield steel or mangalloy — remains the dominant material for automobile shredder wear parts ²⁴. Its durability under impact comes from a unique work-hardening mechanism: the surface hardens progressively under repeated blows, creating an increasingly wear-resistant working layer while the underlying matrix stays tough and ductile. Key performance characteristics:

- Exceptional impact resistance with 30–50% elongation before fracture

- Surface hardness increases with use rather than degrading

- Cost-effective at scale for high-frequency replacement cycles

Mn13 and its Cr-Mo modified variants (Mn13CrMo) remain the default specification for hammers, grates, and anvils across the global automobile shredder installed base.

7.2 High Chrome Cast Iron — Gaining Share in Abrasive Environments

High chrome cast iron (Cr20–Cr26) is gaining traction in shredder applications characterized by fine, highly abrasive feedstock rather than heavy impact loading ²⁷. At a typical hardness of 58–66 HRC, it outperforms manganese steel under pure abrasion conditions, though it is more susceptible to fracture under extreme impact. It is increasingly specified for discharge grates and liner applications where abrasion dominates.

7.3 TiC Composite & Ceramic Insert Parts — The Premium Tier

Wear parts incorporating titanium carbide (TiC) particles or ceramic inserts into a tough steel matrix deliver 2–5× longer wear life than standard manganese steel equivalents ²⁷. The composite structure — an extremely hard insert phase within an impact-resistant matrix — handles the combined abrasion and impact loading of automobile shredder environments. Higher upfront cost is offset by fewer replacements, less downtime, and lower labor cost per ton processed. Advanced ceramic insert casting technology applicable to high manganese steel, high chrome cast iron, and alloy steel substrates is now being deployed by leading Chinese manufacturers to compete with Western premium OEM suppliers ²⁸.

7.4 Bimetallic Castings — Emerging High-Performance Solution

Bimetallic hammers combine a hard high-chrome working surface metallurgically bonded to a tough low-alloy steel base ²⁷. Maximum wear resistance at the impact zone; fracture-resistant toughness at the structural attachment point. As operators in high-throughput facilities shift toward measuring total cost of ownership over purchase price, bimetallic castings are gaining specification traction.

The material evolution trajectory:

Mn13 (Standard) → Mn13CrMo → High Chrome Iron → TiC Composite → Bimetallic / Ceramic Insert

[Baseline cost] [Premium TCO]

8. Downstream Demand Analysis

8.1 Automobile Shredding & ELV Processing

- Approximately 27 million vehicles are recycled globally each year(OICA) ³

- Average vehicle weight: 1,400–1,800 kg, with 65% comprising steel and iron, recoverable at a ~90% rate ³

- Passenger car recycling accounts for 2% of vehicle recycling market sharein 2025 ³

- Overall vehicle recycling rate (reuse + energy recovery): 80–95% of vehicle weight³

- EU mandatory targets: 85% vehicle reuse + 95% recyclabilityper end-of-life unit ¹⁰

- Advanced ASR (automobile shredder residue) processing lines achieve metal recovery rates of 5%²⁹

8.2 Scrap Steel & Ferrous Metal Recycling

Ferrous metals account for approximately 75% of the global scrap metal recycling market by value ², with “old scrap” (post-consumer) contributing roughly 60% of total scrap supply in 2025 ². The automotive sector is growing at the fastest end-use CAGR of 4.7% among all scrap-consuming industries ². Building and construction currently holds the largest end-use share at approximately 38% ², but automotive represents the fastest-growing vector directly tied to shredder operations.

8.3 Non-Ferrous & Aluminum Recycling

The non-ferrous metals recycling segment is expanding at a CAGR of 4.6% through 2035 ². The aluminum scrap market is projected to reach USD 48.6 billion by 2030 (CAGR: 9.8%) ¹⁴. ORNL projects up to 350,000 tons of EV-sourced aluminum body sheet scrap in North America entering recycling streams by the early 2030s ¹⁵. Additionally, 98–99% of automotive batteries are technically recyclable ³, creating new processing requirements for EV battery pack shredding — an emerging application with distinct wear part demands.

8.4 Shredder Equipment Base & Capacity Utilization

- Global primary shredder sales: ~3,300 units in 2025at an average price of USD 122,000 ⁵

- Total production capacity: ~4,000 units annually(~82% capacity utilization) ⁵

- Industry-average gross margins on shredder equipment: ~25%⁵

- The cumulative installed base — growing by ~3,300 units annually — defines the wear parts aftermarket’s long-term growth floor

9. Market Challenges

Scrap price cycles create demand volatility. Scrap metal prices move with steel market cycles, trade policy, and global demand conditions ⁶. When prices contract sharply, recycling operator margins compress and capital expenditure on premium wear part upgrades gets deferred. Operators continue replacing worn parts — but may select lower-grade options until margin conditions improve.

Unplanned downtime amplifies supply chain risk. Automobile shredder operations run on tight throughput schedules where unexpected downtime is immediately costly. Delays in wear part sourcing — whether from shipping disruptions, inventory gaps, or lead-time failures — can force operators to run machines past safe wear thresholds ⁴. This dynamic reinforces the position of suppliers with reliable inventory availability and short delivery windows.

Quality fragmentation in the aftermarket tier. Race-to-the-bottom price competition among some lower-tier Chinese manufacturers has created a quality bifurcation in the aftermarket. Buyers relying solely on price for supplier selection risk part failures, accelerated wear rates, and safety incidents. Certification and material traceability are no longer optional for operators running high-throughput, high-consequence machinery ²⁶.

EV feedstock requires adapted configurations. Electric vehicles introduce material compositions that standard hammermill configurations were not designed to process efficiently: large-format lithium-ion battery packs, high-voltage cable harnesses, and aluminum-intensive body structures. Adapting wear part specifications to these new feedstock profiles requires investment, testing, and supplier collaboration.

Aluminum market volatility affects non-ferrous shredding economics. Recycling Today (April 2026) documented extreme volatility in aluminum markets ³⁰, directly affecting investment decisions in aluminum-focused shredder configurations and the associated wear part procurement planning cycles.

10. Key Opportunities

Ask most shredder operators what keeps them up at night, and unplanned downtime from wear part failures ranks near the top. That conversation is reshaping the opportunity landscape for suppliers in 2026.

EV battery shredding — specifications are still being written. The EV battery recycling segment is generating demand for shredding equipment and wear part geometries that don’t yet have established industry standards. Suppliers with the metallurgical engineering capability to develop application-specific designs for battery-material feedstock are entering a market where technical expertise, not price, is the primary selection criterion.

The TCO argument for premium wear parts is measurable. A hammer set lasting 3,000 hours versus 1,000 hours eliminates two change-out cycles — saving labor, crane time, and the production tons lost during each swap. Suppliers who can document field wear life performance with operator data hold a structural advantage over those competing on unit price alone. TiC composite and bimetallic castings are moving from niche to mainstream in high-throughput operations precisely because the math works.

India and Southeast Asia represent the next capacity buildout. India’s ELV scrapping incentive framework ¹¹ is formalizing a scrapping sector that has historically operated informally. Southeast Asia’s growing automotive fleet — coupled with underdeveloped ELV infrastructure — represents the next frontier for shredder capacity investment. Suppliers already positioned in these markets when the buildout accelerates will capture first-mover procurement relationships.

Predictive maintenance is creating a new revenue model. Wear monitoring sensors and AI-based replacement scheduling are moving from pilot to deployment across larger recycling operations. Wear parts suppliers who integrate into these systems — through IoT-compatible part marking, wear data partnerships, or service contracts — shift from transactional sales to recurring service revenue.

Circular steel policy in Europe will drive sustained throughput demand for a decade. The EU’s circular steel targets — requiring increasing recycled content in automotive, construction, and packaging applications — will sustain shredder throughput growth well beyond 2030 ³¹. European recyclers making capacity investments now to meet these mandates represent a premium, long-term wear parts buyer segment.

11. References

| # | Source | Type | URL |

| ¹ | Business Research Insights — Industrial Shredder Market Report | Market Research | https://www.businessresearchinsights.com/market-reports/industrial-shredder-market-103204 |

| ¹ᵃ | Grand View Research — Metal Shredder Market | Market Research | https://www.grandviewresearch.com/industry-analysis/metal-shredder-market |

| ² | Precedence Research — Scrap Metal Recycling Market | Market Research | https://www.precedenceresearch.com/scrap-metal-recycling-market |

| ³ | Market.us — Vehicle Recycling Market Report | Market Research | https://market.us/report/vehicle-recycling-market/ |

| ⁴ | LinkedIn — US Crusher and Shredder Machine Market | Industry Analysis | https://www.linkedin.com/pulse/united-states-crusher-shredder-machine-market-size-2026-sxuwf/ |

| ⁵ | QYResearch via OpenPR — Primary Shredder Industry Analysis 2026–2032 | Market Research | https://www.openpr.com/news/4445490/primary-shredder-industry-analysis-2026-2032-unlocking |

| ⁶ | Coherent Market Insights — Scrap Metal Recycling Market 2026–2033 | Market Research | https://www.coherentmarketinsights.com/industry-reports/scrap-metal-recycling-market |

| ⁷ | IBISWorld — Scrap Metal Recycling in the US | Industry Report | https://www.ibisworld.com/united-states/industry/scrap-metal-recycling/5391/ |

| ⁸ | LinkedIn — End-of-Life Vehicle Recycling Market Insights | Industry Analysis | https://www.linkedin.com/pulse/end-of-life-vehicle-recycling-market-industry-6uaic |

| ⁹ | Council of the European Union — ST-6759-2026 ELV Regulation | Official Document | https://data.consilium.europa.eu/doc/document/ST-6759-2026-INIT/en/pdf |

| ¹⁰ | Enerpat America — How Are Cars Recycled | Industry Article | https://www.enerpatrecycling.com/how-are-cars-recycled.html |

| ¹¹ | NITI Aayog — Enhancing Circular Economy of ELVs in India | Government Report | https://niti.gov.in/sites/default/files/2026-01/Enhancing-Circular-Economy-of-End-of-Life-Vehicles-ELVs-in-India.pdf |

| ¹² | ShreddingTech — Industry commentary citing Global Recycling Association (2024) | Industry Article (secondary citation) | https://www.shreddingtech.com/blog/how-does-a-scrap-metal-shredder-increase-the-value-of-scrap-metal-recycling.html |

| ¹³ | Yahoo Finance — Non-Ferrous Metal Recycling Market Report 2026 | Market Report | https://finance.yahoo.com/news/non-ferrous-metal-recycling-market-145800159.html |

| ¹⁴ | AWS Marketplace — Aluminum Scrap Recycling Market | Market Data | https://aws.amazon.com/marketplace/pp/prodview-6o3brezmtdsg2 |

| ¹⁵ | ORNL — New Aluminum Alloy for Domestic Auto Supply Chain | Research Report | https://www.ornl.gov/news/new-ornl-aluminum-alloy-strengthen-domestic-auto-supply-chain |

| ¹⁶ | K2 Castings — Metal Recycling Blog | Industry Article | https://www.k2castings.com/category/metal-recycling/ |

| ¹⁷ | LinkedIn / Reports Insights — Europe Industrial Shredder Market | Market Research | https://www.linkedin.com/pulse/europe-industrial-shredder-market-future-developments-forecast-cspjc/ |

| ¹⁸ | Porsche Consulting — ELVs as a Key Resource for the Circular Economy | Consulting Report | https://www.porsche-consulting.com/international/en/publication/elvs-key-resource-circular-economy |

| ¹⁹ | ERTRAC — ELV Recycling in the EU (2026) | Industry Association Report | https://www.ertrac.org/wp-content/uploads/2026/03/ERTRAC-CC-Deep-Dive-ELV-Recycling-2026.pdf |

| ²⁰ | Qiming Casting | Manufacturer Data | https://www.qimingcasting.com/products/shredder-wear-parts/ |

| ²¹ | Huasheng Casting | Manufacturer Data | https://www.hscastings.com/metal-crusher-parts/ |

| ²² | Mayang Casting | Manufacturer (company website recommended for verification) | https://www.mayang.cn/product/scrap-metal-recycling-shredder-wear-parts/ |

| ²³ | Sunwill Foundry | Manufacturer Data | https://www.sunwillmachinery.com/wear-parts/shredder-hammers/ |

| ²⁴ | Wujing Casting | Manufacturer Data | https://www.wjfoundry.com/shredder-parts/ |

| ²⁵ | K2 Castings — Metal Recycling | Manufacturer Data | https://www.k2castings.com/category/metal-recycling/ |

| ²⁶ | Opisimetal — Race-to-the-Bottom Dynamics in Wear-Resistant Castings | Industry Commentary | https://www.opisimetal.com/?gongsi/160.html |

| ²⁷ | CrusherWearPartsPro — Crusher Hammer Material Composition | Technical Article | https://crusherwearpartspro.com/crusher-hammer-material-composition/ |

| ²⁸ | Ceramic insert casting technology — manufacturer technical documentation (specific URL to be verified with manufacturer) | Manufacturer Technical Data | — |

| ²⁹ | ASMCO | Manufacturer Case Study | https://www.amsco.us/products/shredder/ |

| ³⁰ | Recycling Today — April 2026 Issue | Trade Publication | https://www.recyclingtoday.com/fileuploads/audience/issues/2026/4/8/april_recyclingtoday_flipbook-lo.pdf |

| ³¹ | ScienceDirect — Circular Economy & EU Steel Supply Chain | Academic Research | https://www.sciencedirect.com/science/article/pii/S0921344926000492 |

Report compiled: April 11, 2026. All data points are sourced from publicly available market research reports, industry publications, government documents, and manufacturer data as cited. References marked as “unverified primary source” or “secondary citation” should be independently verified before use in commercial, investment, or regulatory contexts. References marked with “—” in the URL field require direct manufacturer verification.